How Canada benefit repayment rules 2026 affect taxpayers

A notice from the Canada Revenue Agency (CRA) stating that a taxpayer owes thousands of dollars can be a difficult experience, especially for individuals who filed accurately and reported all income.

In many cases, these unexpected balances occur due to federal benefit recovery mechanisms, commonly known as clawbacks.

Navigating the shifting thresholds of federal programs is an essential part of personal financial planning in Canada.

The intersection of annual inflation adjustments, updated economic policies, and the rollout of new targeted financial support measures means that understanding the fine print of federal regulations is increasingly important.

For households that received federal support over the past year, learning how Canada benefit repayment rules 2026 affect taxpayers is a practical step toward managing a household budget and preventing unexpected repayment demands from federal authorities.

Key Highlights of the 2026 Benefit Regulations

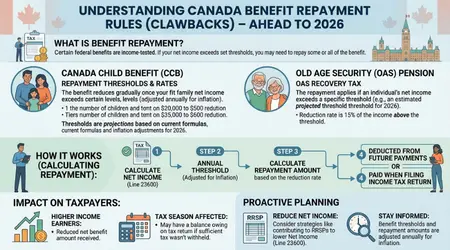

- Threshold Mechanics: Income increases from raises, overtime, or secondary earnings can reduce multiple federal benefit entitlements simultaneously based on Adjusted Family Net Income (AFNI).

- Program Specifics: Employment Insurance (EI) regular benefits require a 30% repayment if net income crosses into the mid-$70,000 range, while Old Age Security (OAS) faces a 15% recovery tax past specific individual limits.

- New Transition: The traditional GST/HST credit structure is transitioning to the Canada Groceries and Essentials Benefit, featuring a 25% ongoing payment boost alongside potential retroactive adjustments for shifting income brackets.

- Proactive Management: Registered Retirement Savings Plan (RRSP) contributions can reduce net income to protect benefit eligibility, while real-time updates to CRA profiles prevent the accumulation of overpayment debt.

How 2026 Thresholds Trigger Benefit Repayments

The administrative structure behind federal social programs relies on a sliding scale determined by a taxpayer’s Adjusted Family Net Income (AFNI).

When household income rises due to salary adjustments, additional hours, or independent contracts, the government systematically reduces corresponding financial benefits.

Because these systems are interconnected, earning beyond a specific threshold can trigger concurrent reductions across several programs.

Employment Insurance (EI) regular benefits operate under strict recovery parameters.

If an individual’s net income for the calendar year exceeds the government threshold, the taxpayer must repay 30% of the lesser of their net income above the limit or the total EI benefits received.

Following annual indexation, this threshold sits within the mid-$70,000 range.

Individuals who experienced temporary unemployment early in the year and subsequently secured higher-paying positions may face repayment requirements if their total annual net income crosses this line.

The Old Age Security (OAS) pension recovery tax operates under a similar framework, affecting seniors who maintain part-time employment or withdraw funds from a Registered Retirement Income Fund (RRIF).

Once individual net income exceeds the designated threshold, a 15% recovery tax is applied to every dollar above the limit.

Because these thresholds undergo annual adjustments based on the Consumer Price Index (CPI), actual exposure depends directly on final net income lines rather than base gross earnings.

++ How Canada caregiver benefit 2026 supports family caregivers

Regulations for the Canada Groceries and Essentials Benefit

A significant structural adjustment to the federal support system involves the sunsetting of the traditional GST/HST credit.

The federal government is fully transitioning to the Canada Groceries and Essentials Benefit.

To facilitate this programmatic shift, the CRA distributed a one-time top-up payment on June 5, 2026, equivalent to 50% of the 2025–26 benefit valuation.

Moving forward, scheduled quarterly payments are adjusted upward by 25% for a five-year period to address ongoing grocery cost pressures.

Eligibility for the June top-up payment depended on the taxpayer’s filed income and family status from the 2024 tax year, matching the criteria used for the January 2026 GST/HST distribution.

However, subsequent quarterly distributions rely entirely on data from 2025 tax returns.

Consequently, households experiencing an income increase between those periods might qualify for the initial June top-up but face disqualification from the subsequent quarterly cycles.

If a CRA reassessment identifies an income or status discrepancy often caused by delayed filing or updates to marital status the agency retroactively applies the new criteria and issues a notice of debt to recover the advanced funds.

Also read: How Auto-Enrollment of Federal Benefits (2026 Onwards) Will Help Low-Income Canadians

Comparative Overview of Federal Programs

Understanding the operational structure of these programs helps tax filers balance baseline financial support with potential administrative repayment risks.

| System Features | Program Adjustments | Repayment Risks & Adjustments |

| Canada Groceries & Essentials Benefit | Features a 25% increase to ongoing quarterly payments; eligible single filers can receive a maximum total of $950. | Subject to retroactive adjustments if 2025 net income increases beyond baseline eligibility limits. |

| Canada Child Benefit (CCB) Scales | Maximum legislative amounts remain protected up to a base family net income threshold of $37,487. | Graduated reduction percentages between 7% and 23% apply to income exceeding the base threshold. |

| EI Benefit Recovery Mechanics | Directs temporary financial safety nets toward lower-income and transitional workers. | Mandates a 30% clawback of received benefits if annual net income exceeds the mid-$70,000 threshold. |

| Home Buyers’ Plan (HBP) Extensions | Extends the temporary grace period before required RRSP withdrawal repayments begin to 5 years. | Omitted annual repayments after the fifth year are automatically added to the filer’s taxable income. |

Case Study: Income Adjustments and Benefit Formulas

A hypothetical scenario demonstrates how Canada benefit repayment rules 2026 affect taxpayers under real-world conditions.

Consider an Ontario household consisting of two parents, Mark and Elena, and two children under the age of six.

In the previous tax year, their Adjusted Family Net Income was $36,000, qualifying them for maximum Canada Child Benefit (CCB) rates and full credit amounts under the previous tax framework.

Over the following year, both individuals increased their working hours and took on additional short-term contracts to manage rising local living expenses. These efforts successfully raised their combined family net income to $65,000.

When the subsequent benefit year begins, the financial impact of the sliding scale formulas becomes apparent.

Because their revised net income of $65,000 sits $27,513 above the base CCB threshold of $37,487, the CRA applies a standard 13.5% reduction formula for families with two children.

- CCB Reduction Calculation: Multiplying the excess income of $27,513 by the 13.5% reduction rate results in a $3,714 annual decrease in child benefit entitlements.

- Grocery Benefit Adjustments: This revised income level also places the household past the threshold for the upcoming quarterly Canada Groceries and Essentials Benefit, removing eligibility for that specific program.

Because federal benefit distributions are recalculated every summer and paid out incrementally over the subsequent 12 months, the household’s monthly cash flow declines by approximately $350 beginning in July.

For taxpayers in similar income brackets, utilizing legal, tax-deductible financial tools can modify net income figures prior to the conclusion of the tax year.

Preventive Measures Against Unexpected Tax Debts

Taxpayers have access to established mechanisms to manage their net income figures and minimize potential benefit repayments.

The primary tool for adjusting these calculations is the Registered Retirement Savings Plan (RRSP).

Because the CRA determines benefit eligibility based on net income rather than gross earnings, documented contributions to an RRSP reduce a filer’s net income dollar-for-dollar.

Had a household in Mark and Elena’s situation allocated a portion of their increased earnings into an RRSP, their adjusted family net income would have declined closer to the base threshold.

This adjustment can lower immediate tax liabilities while preserving eligibility for monthly CCB distributions and related grocery benefits.

Furthermore, maintaining accurate, real-time profile updates with the CRA is critical.

Reporting changes in marital status, dependents, or significant income drops through the CRA My Account portal allows the agency to adjust monthly distributions accurately.

This proactive reporting prevents the accumulation of substantial overpayments that must be repaid during future tax cycles.

Managing personal finances effectively requires monitoring how changes in total earnings affect baseline benefit thresholds.

By keeping track of net income lines and utilizing strategic deductions, individuals can maintain stable household budgets and better understand how Canada benefit repayment rules 2026 affect taxpayers throughout the fiscal year.

Frequently Asked Questions

Why does the CRA require the repayment of automatically distributed benefits?

The CRA issues advanced monthly or quarterly benefit payments based on historical income data from previous tax filings.

If a taxpayer’s income increases substantially during the current calendar year, their legal entitlement drops.

The resulting variance is classified as an overpayment, creating an official balance owing on the taxpayer’s account.

Does the temporary federal gas tax suspension influence benefit calculations?

No. The temporary reduction of federal fuel excise tax rates to zero cents per litre, scheduled to run until September 7, 2026, reduces costs directly at the pump.

Because it does not alter a taxpayer’s net income lines, it operates independently of federal benefit calculations and does not trigger clawback mechanisms.

What administrative options exist if a benefit debt cannot be paid immediately?

Taxpayers who receive a notice of debt that exceeds their current financial capacity can contact the CRA to discuss administrative options.

The agency routinely establishes formalized “payment arrangements” to clear outstanding balances over a set period.

Alternatively, the CRA may automatically withhold future benefit payments until the debt is fully recovered.

Can provincial credit programs be adjusted alongside federal benefits?

Yes. Most provincial support programs, such as the Ontario Trillium Benefit, rely directly on federal tax return data and net income metrics to calculate regional credits.

Consequently, a rise in net income can trigger simultaneous reductions in both federal and provincial benefit allocations.